For over a decade, the recipe for investment success seemed simple: own the giants. Large-cap growth stocks propelled markets to historic heights, rewarding those who stayed the course. But today’s success has quietly created tomorrow’s vulnerability.

If you look under the hood of your portfolio, you might find you are far less diversified than you think. As of January 2026, the top 10 stocks in the S&P 500 account for nearly 40% of the entire index. This level of concentration means that even if you own a “diversified” index fund, your financial future is increasingly tied to the fate of just a handful of companies.

The myth of permanent dominance

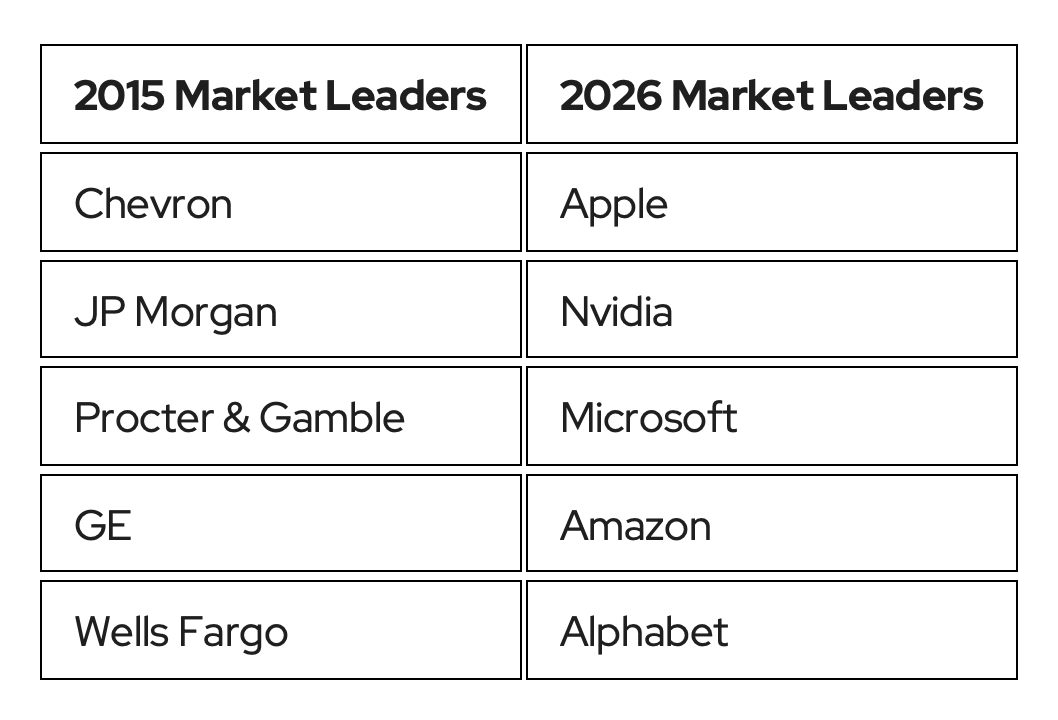

History is a harsh teacher when it comes to market leadership. The “untouchable” blue chips of yesterday are rarely the leaders of today. Consider how the market’s “DNA” has shifted in just ten years:

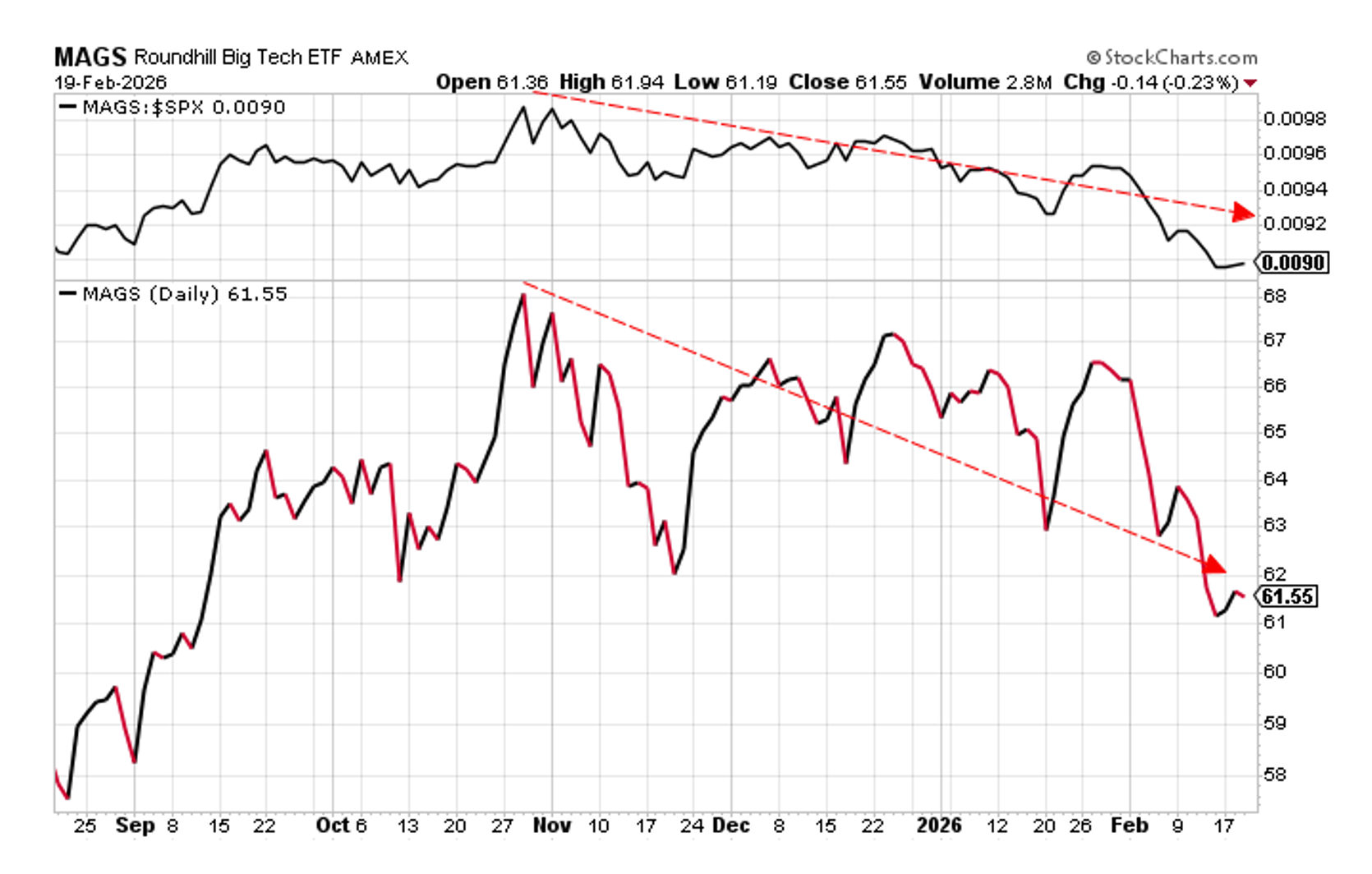

The chart below illustrates the performance of an ETF tracking the ‘Magnificent 7. The ‘Magnificent 7’ has hit a plateau. Since peaking in late October, these equal-weighted positions have stalled and has since lagged the broader market. This suggests that the era of effortless growth in concentrated tech may be reaching a turning point.

The question isn’t whether these are good companies — they are. The question is whether you can afford the risk if they stop being great. Even the most dominant firms struggle to maintain meteoric growth forever; history shows they often fade after their first decade of dominance. In the worst-case scenario, an unmanaged concentrated position can lead to catastrophic loss.

Escaping the “binary trap”: To hold or to sell?

If you hold a large position resulting from the explosive growth of the last decade, congratulations — you’ve cleared a major hurdle in wealth creation. But the “what now?” can feel paralyzing. Most investors feel stuck in a binary choice:

- The “Hold” strategy: Keep the position, pray for continued growth, and stomach gut-wrenching volatility.

- The “Sell” strategy: Liquidate the position and immediately hand over a massive percentage of your hard-earned wealth to the IRS in capital gains taxes.

At Signet, we believe there is a third way. Managing a concentrated position should not be a forced choice between market risk and tax hits.

Sophisticated strategies for concentrated wealth

We look beyond the “buy or sell” mentality by asking two critical questions:

- Where would you invest today if taxes weren’t a factor?

- How large is this position relative to your total net worth?

Based on your unique profile, we deploy three primary tools to transition from concentration to true diversification:

1. Direct indexing

Instead of buying a mutual fund or ETF, we buy the individual stocks within an index for you. This allows us to tax-loss harvest at the individual stock level — using losses from specific companies to offset the capital gains triggered by selling your concentrated position.

2. Option overlays

For investors not ready to sell, we use hedging strategies (such as protective puts or collars) to floor your downside. This allows you to retain the stock and participate in some upside while mitigating the risk of a price collapse.

3. The hybrid approach

For the largest positions, we often combine both. We may liquidate a portion of the stock to fund a Direct Indexing account (generating future “tax alpha”) while simultaneously hedging the remaining shares with an Options Strategy. This creates a multi-year exit plan that protects your principal and your tax bill.

Take the next step

Concentration builds wealth, but diversification preserves it. Don’t let a decade of historic returns be erased by a lack of planning. Contact us today to schedule your personalized concentration risk assessment.

IMPORTANT DISCLOSURE

This material is provided for informational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any security or investment product. All investing involves risk, including loss of principal. Private credit investments are illiquid and suitable only for qualified investors who can bear these risks. Past performance is not indicative of future results.