Owing money to the IRS can be stressful, but you have options to help you repay your tax debt. One such option is setting up an IRS payment plan, while the other is taking out a personal loan.

Pros of IRS payment plans

- Lower interest and fees compared to personal loans

- Up to 72 months to pay off your tax bill

- Avoid taking on additional loans

Cons of IRS payment plans

- Limits apply for long-term plans (owed amount must be under $50,000)

- Set-up fees may apply

- Dealing with the IRS bureaucracy can be time-consuming

Using a personal loan to pay taxes

Another approach to settling your tax debt is by using a personal loan. This straightforward option provides fixed interest rates, fixed monthly payments, and a clear repayment plan.

Pros of personal loans

- Quick online application and funding process

- Opportunity to choose terms that suit your needs

- Avoid dealing directly with the IRS

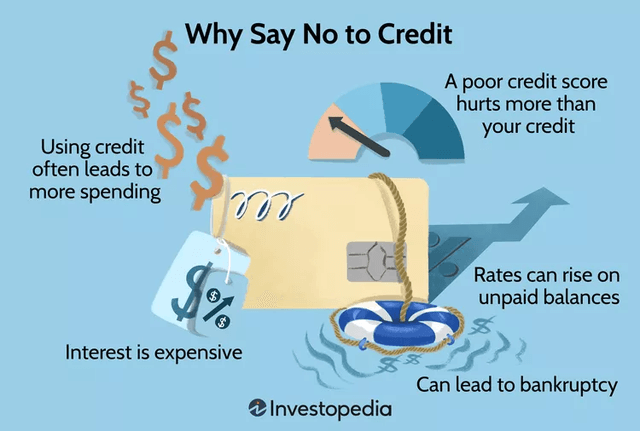

Cons of personal loans

- Total loan costs might be higher than IRS payment plans

- Possible impact on your credit score

- Borrowing more money can come with risks

Other payment options

If you’re considering alternatives, you can pay your taxes with a credit card, but beware of high-interest rates. Another option is a 401(k) loan, but be mindful of repayment terms and potential penalties.

Do IRS payment plans affect your credit?

IRS payment plans do not affect your credit or get reported to credit bureaus.

The bottom line

Handling IRS debt promptly is essential to avoid accruing more interest and fees. Whether you choose an IRS payment plan, a personal loan, or explore other options, each approach has its advantages and costs. Consider your financial situation carefully before deciding on the best course of action.