Divorce can be an emotional roller coaster, one you never wanted to ride and one you can’t wait to get off. While you’re holding on tight and waiting for this shaky ride to end, it’s easy to forget about basic money management and how important it will soon become, particularly when it comes to your personal credit. If you don’t protect yourself, you risk the negative consequences associated with your former spouse’s debt.

1. Close it: Get rid of entangled credit and cards.

As you begin to work toward de-tangling the financial web that you and your spouse have woven over the years, a good first step towards independence is to close any joint lines of credit, joint credit cards, and even joint checking accounts.

2. Freeze it: Put your credit on ice.

Even if it seems unlikely, your spouse might be able to open new lines of joint credit without your authorization.

3. Separate it: Create a line of credit just for you.

Even if you have been married for a long time, the credit bureaus maintain separate files and credit ratings on you and your spouse. That is why creating separate lines of credit now is vital.

4. Monitor it: Check regularly to stay on top of it.

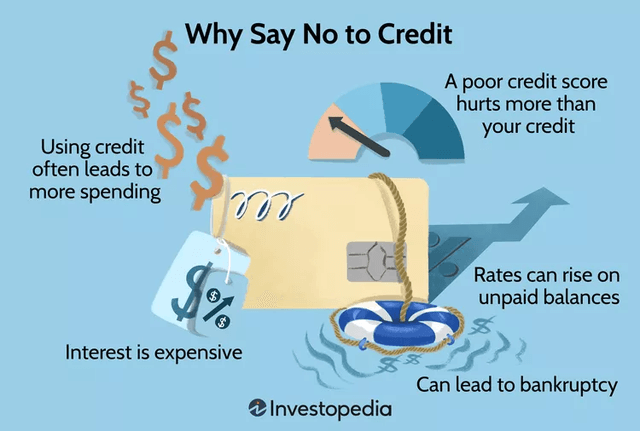

Bad credit can cost you money in ways you never imagined — including unfavorable interest rates when you take out a mortgage, car loan, or student loan. It could keep you from being able to rent an apartment, it could even prevent you from landing that great new employment opportunity you were applying for.

Remember that no divorce decree trumps the contract you have with the issuer — this means that even if your divorce settlement states that your spouse must pay the debt on a joint credit card, your credit is still at risk if they choose not to pay.

These are four tactics to help you protect yourself from the risk of being tied into your former spouse’s debt. Taking the time to educate yourself about your personal credit will bring you closer to the resolution of your dissolution.