US economics, inflation, jobs and the Fed

The Federal Reserve held its benchmark short-term interest rate in the range of 3.50% to 3.75% at the Federal Open Market Committee (FOMC) meeting on January 28th. The pause will give Fed officials the opportunity to assess additional inflation and jobs data. The current Fed interest rate has moved closer to the estimated neutral level, which is the rate where the Fed’s policy is neither stimulating nor restricting the economy. At that level, it’s possible for growth to take place with stable inflation according to Value Line.

The U.S. economy does not need near-term stimulus from interest rates or from the government putting additional cash into circulation. The nation’s gross domestic product (GDP) expanded by estimated annualized rates of 3.8% and 4.3% in the second and third quarters of 2025, respectively. The consensus is that the final quarter probably exceeded the previous forecast of around 2%, fueled by a record retail holiday sales season and a slowly improving manufacturing sector. On the latter front, industrial production advanced in both November and December, and surveys of manufacturing activity in the New York and Philadelphia areas showed notable gains last month.

Meanwhile, geopolitical concerns have increased. In addition to the ongoing unrest in Iran, the financial markets were roiled by bickering over Greenland, which President Trump wants to acquire from Denmark for national security reasons. We follow the situation closely and it looks like the preliminary agreement has been reached between all interested parties.

Global economy

The signal of normalizing business sentiment is reinforced by the available readings from January regional Fed surveys, which are pointing to a sharp rise in US business expectations as we turn into the new year according to JP Morgan (JPM).

The willingness of households to spend through labor market weakness is an important driver of the rebound in business sentiment. The news on this front remains constructive outside China. JPM’s Euro area consumption now-caster is tracking a pickup to a 1.5% annual rate gain last quarter while this week’s delayed US October-November PCE release lifted JPM’s tracking for 4Q25 consumption to a robust 3.1% annual rate gain. Normally, rapid US consumption gains generate positive dividends for the rest-of-world but trade flows through October point to sharp declines in US consumer goods imports.

With solid gains in final sales during 2H25 accompanied by a large positive net trade contribution, US GDP growth is projected to have surged to a 3.7% annual rate. JPM downplays the importance of this net trade contribution, which is likely to be reversed or revised away, and see the 2.4% annual rate gain in 2H25 private final demand as a better gauge of the growth momentum the economy is carrying into the new year.

Stock market

Fourth-quarter earnings season got off to a solid start. The consensus forecast is calling for profit growth of around 8% for the S&P 500 companies. If realized, this would mark the 10th consecutive quarter of growth for the index companies.

Professor Siegel shares our enthusiasm about the markets:

“Earnings season has reinforced this constructive backdrop. While individual stocks are seeing mixed responses largely on 2026 guidance uncertainties, the aggregate picture is reassuring. There is no evidence of deterioration in consumer spending or labor markets, and corporate profits are holding up well. Importantly, leadership within the equity market is broadening. Small-cap stocks and value stocks are meaningfully outperforming in 2026, marking one of the strongest relative runs for value since the growth-led bull market began several years ago. This rotation is consistent with my view that beneficiaries of artificial intelligence are primed to become consumers and users of AI, not just its producers.

In fixed income, credit fundamentals look solid, but total returns are constrained by duration risk. Spreads have compressed sharply, particularly in agency MBS, partly reflecting policy actions. Still, from a broader macro perspective, the bond market is simply moving back to a normal term structure. Historically, the 10-Year Treasury yield has averaged about 110 basis points above the fed funds rate. If the 10-year holds near 4¼%, that implies fed funds in the low 3% range over time — roughly two additional 25-basis-point cuts. I would only grow concerned on implications for the equity markets if the 10-Year were to move decisively above 5%, which could signal fiscal stress. We are not there.

Taken together, the past week reinforces my optimism for the year ahead. Growth is strong, productivity is improving, inflation is contained, and markets are broadening beyond last cycle’s narrow leadership. While noise around policy and geopolitics will persist, the fundamental trajectory for both the economy and markets remains firmly positive.”

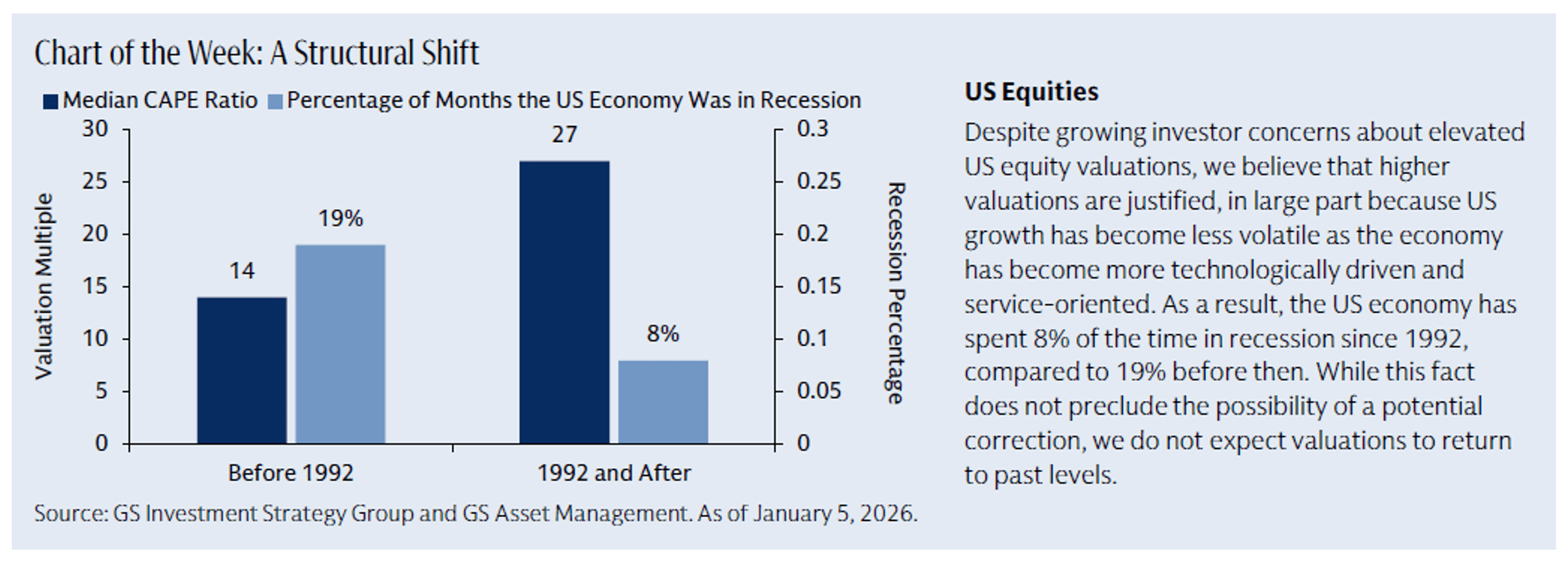

In their latest edition of Market Monitor Goldman Sachs reinforces Professor Siegel’s reasoning:

The information and opinions included in this document are for background purposes only, are not intended to be full or complete, and should not be viewed as an indication of future results. The information sources used in this letter are: WSJ.com, Jeremy Siegel, Ph.D. (Jeremysiegel.com), Goldman Sachs, J.P. Morgan, Empirical Research Partners, Value Line, BlackRock, Ned Davis Research, First Trust, Citi research, HSBC, and Nuveen.

IMPORTANT DISCLOSURE

Past performance may not be indicative of future results.

Different types of investments and investment strategies involve varying degrees of risk, and there can be no assurance that their future performance will be profitable, equal to any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

The statements made in this newsletter are, to the best of our ability and knowledge, accurate as of the date they were originally made. But due to various factors, including changing market conditions and/or applicable laws, the content may in the future no longer be reflective of current opinions or positions.

Any forward-looking statements, information, and opinions including descriptions of anticipated market changes and expectations of future activity contained in this newsletter are based upon reasonable estimates and assumptions. However, they are inherently uncertain, and actual events or results may differ materially from those reflected in the newsletter.

Nothing in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice. Please remember to contact Signet Financial Management, LLC, if there are any changes in your personal or financial situation or investment objectives for the purpose of reviewing our previous recommendations and/or services. No portion of the newsletter content should be construed as legal, tax, or accounting advice.

A copy of Signet Financial Management, LLC’s current written disclosure statements discussing our advisory services, fees, investment advisory personnel, and operations are available upon request.