US economics, inflation, and the Fed

The Federal Reserve lowered the benchmark short-term interest rate by a quarter point at its September monetary policy meeting. This was the first action from the Federal Open Market Committee (FOMC) since last December. While policymakers are still watching the pace of inflation, a bigger concern right now for the lead bank is declining job growth. The August retail sales gain of 0.6% was double the expectation, indicating consumers are spending.

However, the September Consumer Sentiment Index fell 21% year over year, with survey respondents showing concern about a weakening labor market and higher prices due to tariff policies according to Value Line. The state of the consumer sector will likely play a huge role in how aggressively the central bank cuts interest rates.

Professor Siegel notes:

“I expect 25 basis point cuts on October 29 and in December, and another 50–75 basis points by early next year as the Fed moves toward a more neutral stance. The 10-year rate should remain range-bound near 4% with a modest term premium; mortgage spreads can narrow further.”

Indeed, while housing remains weak, mortgage rates are falling faster than the 10-year rate would suggest because the pandemic-era origination premium is compressing. That premium can still recede further, allowing 30-year fixed rates to decline even if the 10-year rate hovers around 4.0%-4.1%. That’s a direct tailwind to housing turnover and construction sentiment as we move through Q4 according to Professor Siegel.

In the meantime, as mentioned above, the labor market is weakening. This was reflected in several key data points, including minimal job gains this summer. The unemployment rate ticked higher, to 4.3% in August, while the labor force participation rate remains low. This suggests increasing slack in the labor market according to Value Line. It also should be noted that a recent report from the Bureau of Labor Statistics showed that U.S. employers added far fewer jobs than originally thought in 2024 and 2025. For the 12-month period ended March 31st, payroll totals were revised lower by 911,000 jobs.

So, it is apparent that the U.S. economy is slowing. The Congressional Budget Office (CBO) is estimating that gross domestic product (GDP) will advance 1.4% this year, which would be half the 2024 rate. The CBO cited reduced immigration — and its impact on the supply of labor — along with tariffs as the primary reasons for its lower GDP forecast. That said, it remains to be seen if the CBO is underestimating the possible positive impact of the new budget bill, which includes tax cuts and regulation rollbacks, on GDP.

Global economy

JP Morgan (JPM) sees two reasons not to extrapolate recent growth resilience or embrace the Goldilocks signal from risk assets. First, a slower and more differentiated roll out of the trade war has encouraged a more extended front-loading of activity and delayed its pass through to US consumer prices. The observed US tariff rate stood below 10% in July — roughly half the level JPM expects it to reach – and US goods imports have yet to drop relative to their trend pace. The main beneficiaries of these developments have been Asian tech exporters and US consumers. Indeed, US goods prices rose only a modest 0.4% annual rate in the first seven months of this year.

Trade war drags appear to be building. Asian export gains have stalled on the back of recent weakness in China and August readings elsewhere point to the beginning of a turn with contractions reported in the Asean group (Singapore, Malaysia, and Vietnam). Taiwan shipments continue to outperform, with August exports surprising yet again to the upside. Even here, though, manufacturing has stalled in the three months through July.

Meanwhile, upward pressure on U.S. goods price inflation is building. Fading energy price declines are set to combine with sustained upward pressure on food prices to push the headline CPI higher. Tariff pass-through and rising pre tariff import prices (reflecting this year’s dollar slide) are now boosting core goods price inflation.

Slowing Asian exports and rising US consumer price inflation do not, by themselves, provide a strong indication about the growth. Instead, JPM’s primary hesitancy in embracing positive momentum is concern around the behavioral signal coming from developed markets business. Global growth has been supported this year by strong business investment spending that appears to be continuing this quarter. However, developed markets’ job growth has slid to a stall. Capex spending growth can be volatile and tends to be sensitive to near-term growth shocks.

At the same time, mature expansions tend to see job growth hold up in the face of shocks perceived to be transitory. There are two large structural factors — AI technology diffusion and weakening immigration flows — which may contribute to the current unusual signals from business.

But at least in the US, the breadth and slowing employment across sectors and job types suggests that labor markets are signaling a broad shift in business caution, even as narrowly based gains in capex support growth. Nevertheless, JPM expects the global economy to grow by 2.5% this year.

Stock market

While many market participants expect small and mid-caps, rate-sensitives, and high-quality dividend payers to catch up, the AI wave keeps Mega Caps dominating so far this year. Professor Siegel expects a rotation that lifts the broader market breadth into year-end if we get the “sea change” of two more cuts this year. The risks — an upside surprise in payrolls, a claims drift to 250k+, or a sudden tariff-driven supply pinch — would alter the pace, not the direction, of easing.

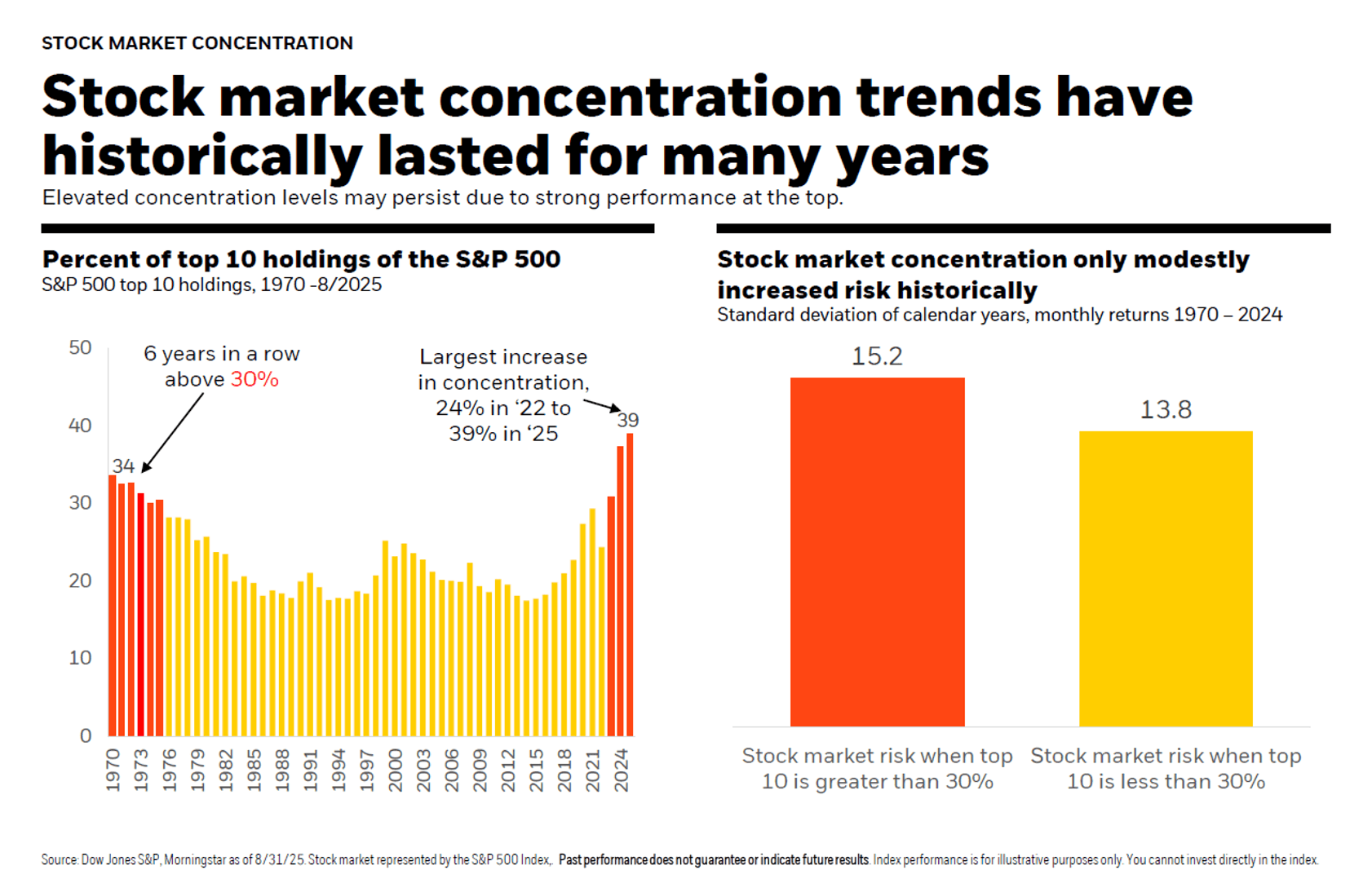

In their September Student of the Market publication, BlackRock suggests that concentrated leadership is nothing new to the market and it can last for many years (See the Stock Market Concentration Illustration below):

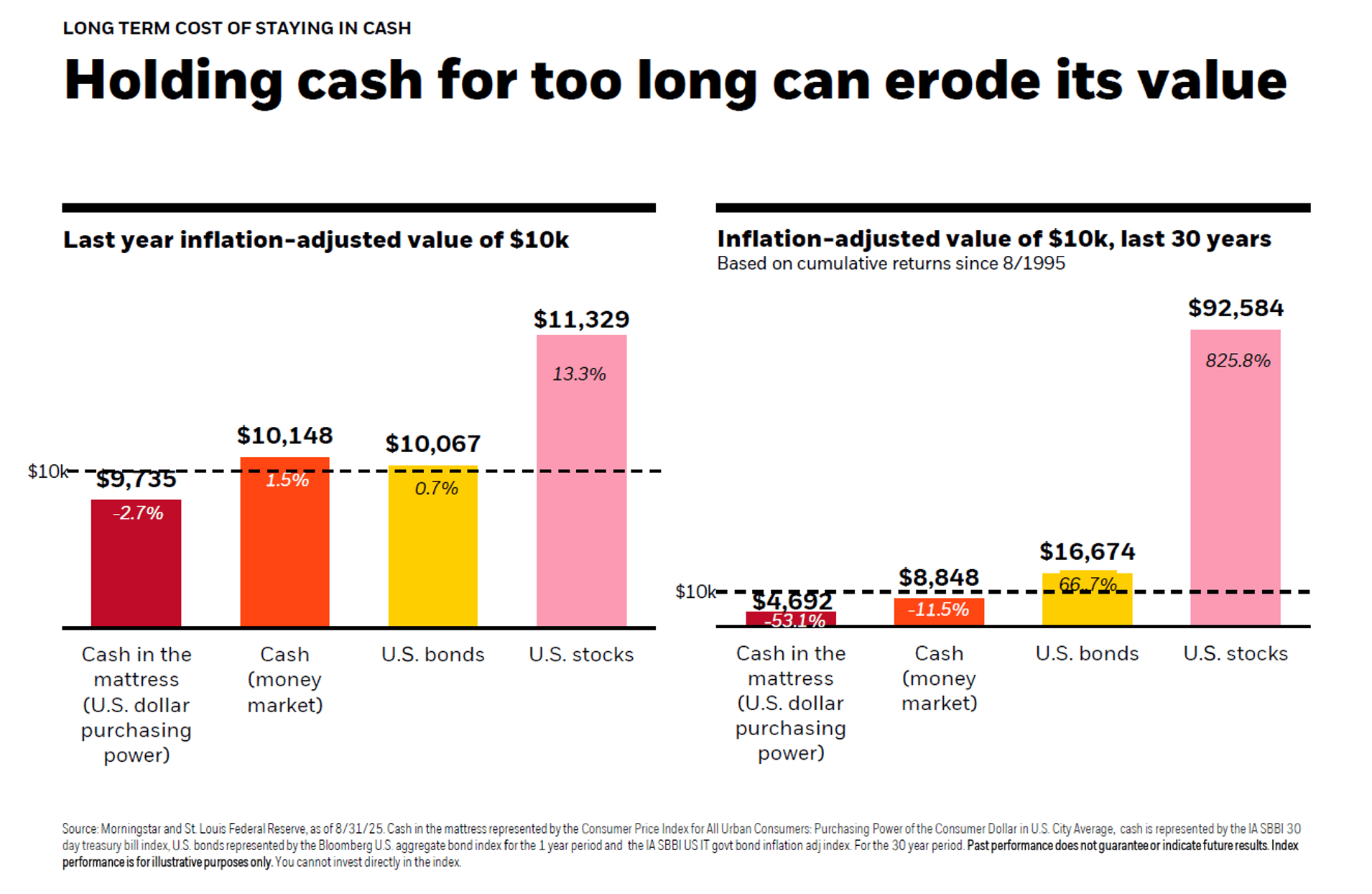

However, while it is important to pay attention to higher valuation of the aggregate market, it is crucial to remember that the higher valuations are currently justified by enormous amount of cash flow and profitability produced by Mega Caps and the market in general. Moreover, while $7.7 trillion in cash equivalents on the sideline represent a huge buying power, hesitant investors need to realize that by holding cash they are eroding its value according to BalckRock’s September Student of the Market illustration below. Staying invested is much more beneficial.

The information and opinions included in this document are for background purposes only, are not intended to be full or complete, and should not be viewed as an indication of future results. The information sources used in this letter are: WSJ.com, Jeremy Siegel, Ph.D. (Jeremysiegel.com), Goldman Sachs, J.P. Morgan, Empirical Research Partners, Value Line, BlackRock, Ned Davis Research, First Trust, Citi research, HSBC, and Nuveen.

IMPORTANT DISCLOSURE

Past performance may not be indicative of future results.

Different types of investments and investment strategies involve varying degrees of risk, and there can be no assurance that their future performance will be profitable, equal to any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

The statements made in this newsletter are, to the best of our ability and knowledge, accurate as of the date they were originally made. But due to various factors, including changing market conditions and/or applicable laws, the content may in the future no longer be reflective of current opinions or positions.

Any forward-looking statements, information, and opinions including descriptions of anticipated market changes and expectations of future activity contained in this newsletter are based upon reasonable estimates and assumptions. However, they are inherently uncertain, and actual events or results may differ materially from those reflected in the newsletter.

Nothing in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice. Please remember to contact Signet Financial Management, LLC, if there are any changes in your personal or financial situation or investment objectives for the purpose of reviewing our previous recommendations and/or services. No portion of the newsletter content should be construed as legal, tax, or accounting advice.

A copy of Signet Financial Management, LLC’s current written disclosure statements discussing our advisory services, fees, investment advisory personnel, and operations are available upon request.